By Jonathan Harner, CFP®

Planning for the future is something most people know they should do, but they might not know exactly what to do—or how to get started. This is where financial planners can add significant value. We can assess your current financial situation, identify long-term goals, and create a path toward success. But many people find it difficult to commit to a working relationship with a financial planner when they don’t actually know what the end product will look like.

Visualizing a service can be challenging; it’s not as tangible or clear-cut as an insurance policy or other financial product. Because of this, it can be hard to conceptualize what you are buying when you invest in a financial plan. Many advisors simply want to sell you a product and collect a fee on your assets. At Wichita Wealth Management, we want to be your trusted advisor as you navigate the ever-changing landscape of your financial situation. As such, we’ve put together this sample financial plan that outlines some of the deliverables we provide to our clients to offer value, clarity, and confidence throughout the year.

What Does a Financial Plan Include?

First, you may be wondering about what goes into a holistic plan. Financial plans often address a myriad of concerns and goals, from tax planning to retirement income strategizing. Depending on your needs, your plan may narrow in on one element or address multiple goals you’d like to pursue over time. Whatever you choose to focus on, your financial plan is designed to serve as your road map, helping you pull all the moving parts of your finances together so you can navigate the years before, during, and after your transition to retirement.

We believe a good financial plan should give you a detailed, complete view of your current financial situation, a thorough modeling of where you want to be, and the actions you need to take to reach those goals. It should address all the pieces of your financial puzzle, from stresses and fears to your values and dreams, and include risk factors, cash flow, retirement, estate planning, taxes, education, and income strategies to help bring you clarity and guidance. It is through our planning process that we help you prepare for life’s expected and unexpected circumstances.

The result is a simple yet powerful road map to guide you toward financial freedom.

See a Sample Financial Plan

We’ve developed a sample financial plan that reflects our planning process. It looks at a fictional person’s lifestyle income plan and how we developed it, including identifying their goals, creating a net worth statement, reviewing their income buckets, investments, and more.

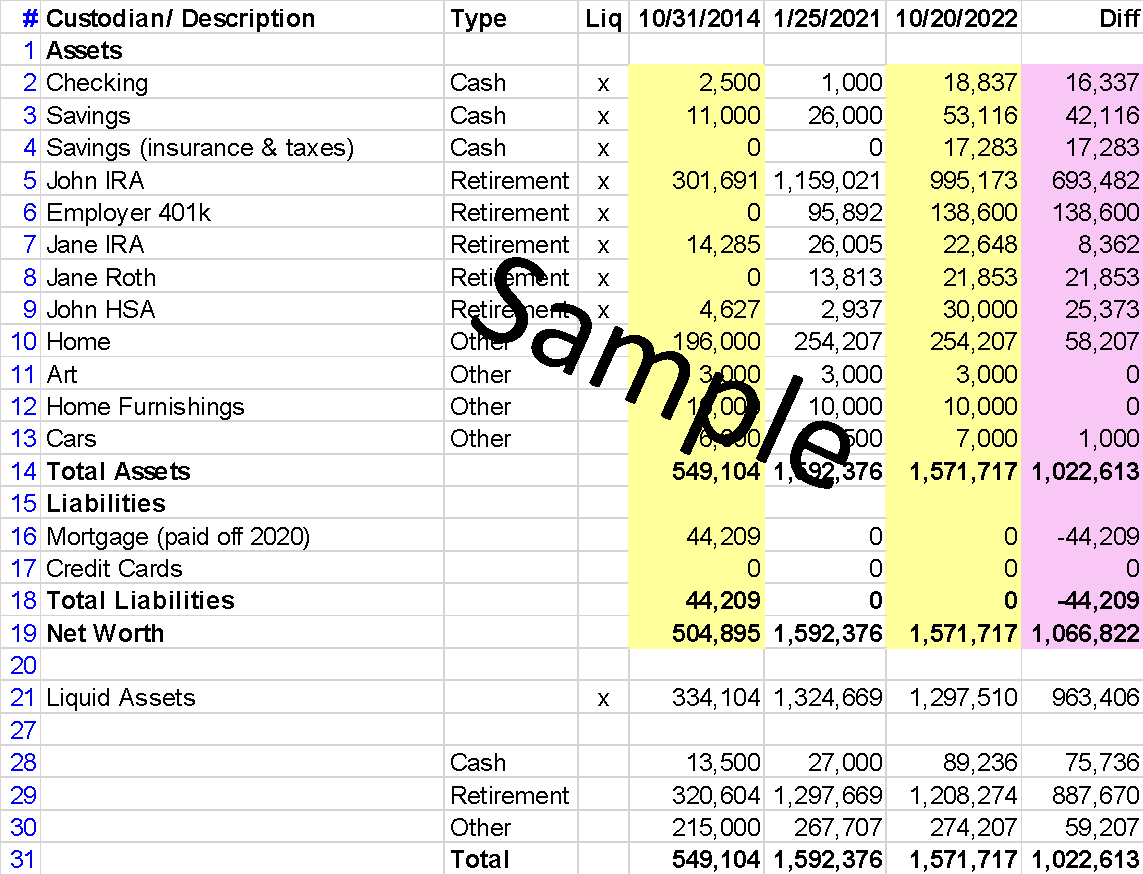

Net Worth Statement

The first thing we look at is the net worth statement. This provides clarity on your overall financial picture and helps answer questions like: Where is most of your wealth? Do you have enough cash in the bank, or too much? How much debt do you have? These critical components of assessing financial wellness will be the starting point for any financial plan. In the case of John and Jane, our sample clients, you can see that their net worth grew from $979,554 to over $1.1 million in the 5 years that we were working together. This is a great sign that a financial plan is working.

Income Buckets

Because John and Jane are planning for retirement, it’s crucial that we review their income buckets. These help us better understand how much income a client needs to fund their retirement, and when (if ever) they will need to alter their spending habits to make the plan sustainable. Once we have these numbers, we can create a customized investment plan to help you generate the income you need in retirement.

Since we know that market downturns are a matter of when, not if, we segregate funds into three different risk-adjusted buckets. In John and Jane’s case, we determined that they should keep no less than $97,000 in highly liquid cash assets. This is a contingency fund to be used in case of an emergency or unforeseen circumstances so they don’t have to liquidate their other investment holdings at inopportune times in the market. The second bucket is income. These are income-producing investments like bonds, or dividend-paying stocks, that will generate the bulk of the funds for John and Jane’s everyday retirement expenses. Lastly, we have the growth bucket, which will be invested in higher-risk, higher-return assets that can generate capital appreciation. This bucket would be used for longer-term goals like legacy planning or expenses in the later years of retirement.

Social Security Strategy

Social Security claiming decisions are complex and should not be made lightly. Many clients don’t realize how much money they could be leaving on the table by claiming benefits just a couple of months early. With our financial planning software, we can calculate the difference in the lifetime benefit you will receive based on different claiming decisions. As you can see in the table below, John and Jane will receive substantially more income if they both delay benefits until age 70.

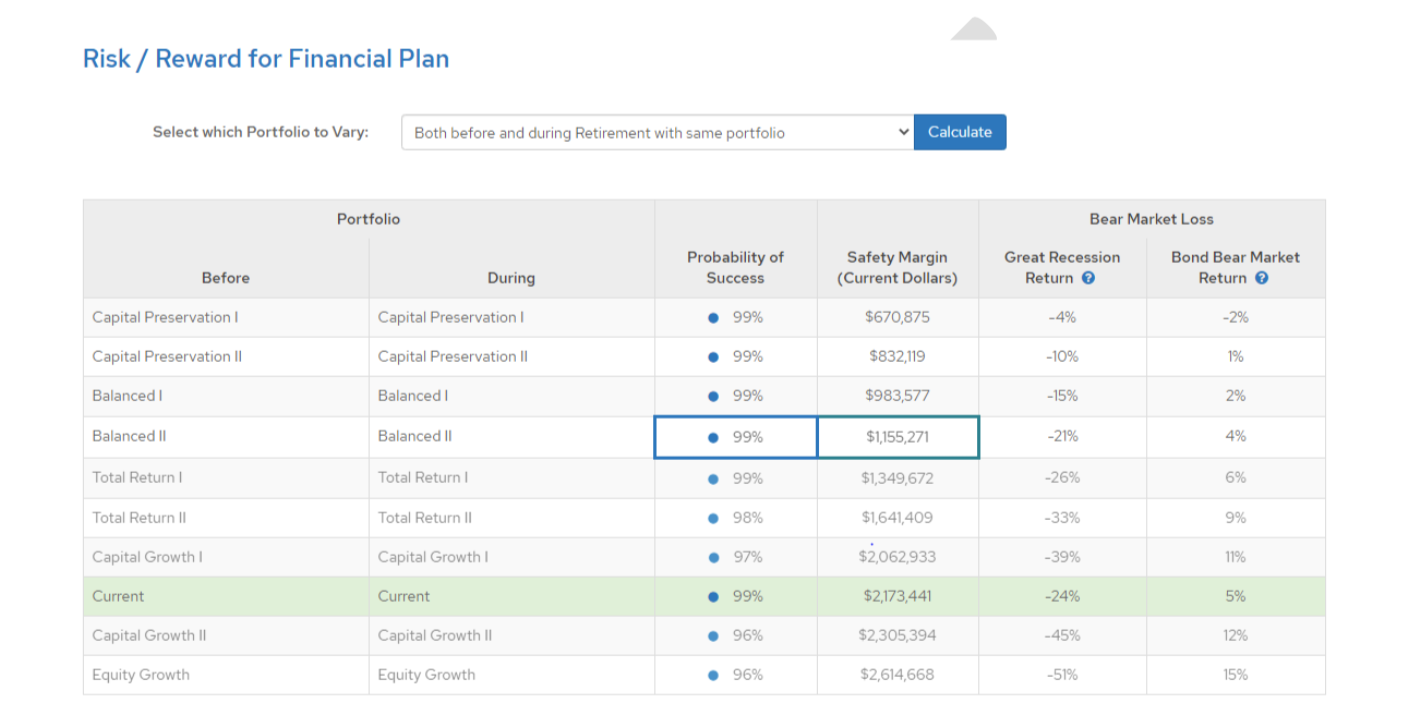

Investment Analysis

Next, we look at a detailed analysis of the different investment options available to each client. The chart below shows several investment strategies ranging from conservative (capital preservation) to aggressive (equity growth). Each option has a probability of success and potential returns during down markets. We find this helps us hone in on a client’s risk tolerance and help them select the best portfolio for their unique needs. In the case of John and Jane, the Balanced II portfolio makes the most sense from a risk-reward perspective. Not only do they reduce their risk substantially, but they also maintain a 99% probability of success.

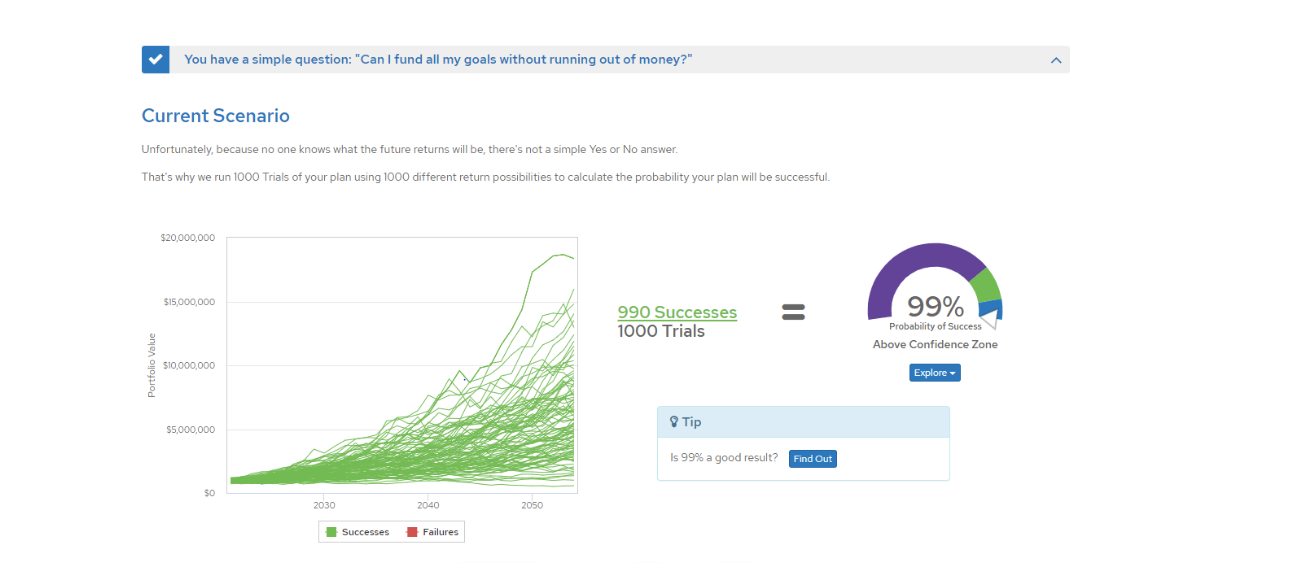

Monte Carlo

Lastly, we look at a Monte Carlo analysis to run simulations on the proposed plan. If the client implements our recommendations, will they run out of money in retirement? In John and Jane’s case, they have a 99% probability of success with the recommendations we developed.

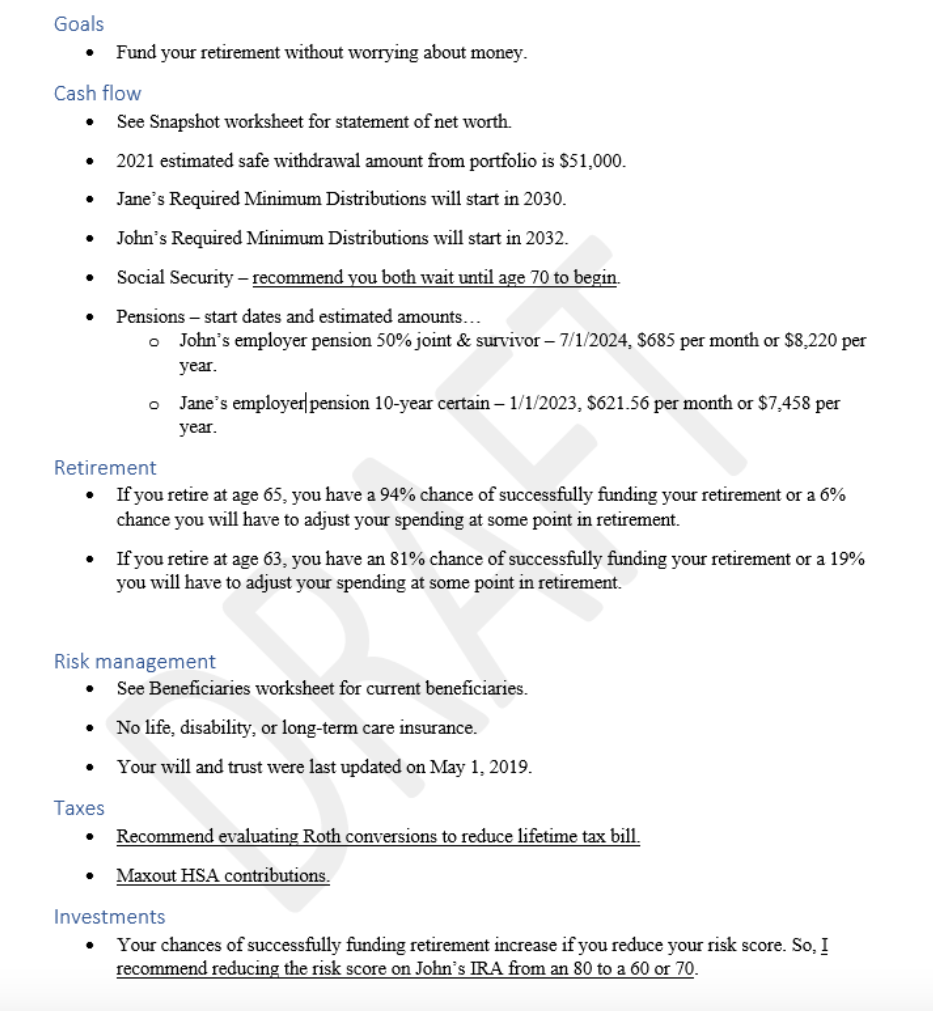

One-Page Financial Plan Summary

Since financial plans tend to be big and bulky, we like to provide our clients with a one-page executive summary that details the most important points they need to keep in mind. This is a quick way to reference the plan in between our regular meetings. It helps clients to keep track of the recommendations and stay accountable throughout the entire planning process.

Keep in mind that this is only a hypothetical plan presented to illustrate what a client’s plan may resemble should they work with us. The characters and circumstances are completely fictional and are for illustrative purposes only. Be sure to seek the advice of a qualified professional for your particular situation and do not rely upon any of the information herein to make personal financial decisions.

Take a look through the full sample plan here to see how our proven process helps you pursue your goals and financial freedom. Once you’ve reviewed it, schedule a free consultation today by clicking here and we can discuss further how we can create a tailored financial plan for you.

About Jonathan

Jonathan Harner is a CERTIFIED FINANCIAL PLANNER™ practitioner at Wichita Wealth Management, a fee-only, fiduciary financial advisory firm dedicated to helping their clients thoroughly prepare for retirement. Jonathan’s goal is to simplify the complex so his clients can experience confidence and peace of mind as they work toward and live out their retirement dreams. He specializes in developing and implementing tax strategies that maximize his clients’ money and builds a tax-efficient withdrawal plan for retirement. Jonathan loves finding opportunities for his clients to save money and is dedicated to continual learning and growing in his profession so he can provide solutions for his clients’ financial needs. When he’s not working, you can find Jonathan spending time with his wife, Annie, and their daughter, staying active in his church community, and participating in his two favorite (but vastly different) hobbies: CrossFit and Dungeons & Dragons. To learn more about Jonathan and how he can help you, connect with him on LinkedIn.